Slow Dancing in a Burning Room

Covid has created vastly different points of view, and it’s given people lots of time to sit on the internet. It’s a different world, and you ignore how much has changed at your own expense.

Capital Thinking • Issue #767 • View online

The demand for forecasts grows after a surprise. It’s quite an irony.

Surprises make you feel like you’re not in control, which is when it feels best to grab the wheel with both hands, listening to those who tell you what happens next despite being blindsided by what just happened.

Two Worlds: So Much Prosperity, So Much Skepticism

Morgan Housel | The Collaborative Fund Blog:

That’s where we are with Covid and the economy. Ten months after the surprise of our lifetimes, everyone wants a clear map of the future.

Who wins? Who loses? When will travel recover?

Will work be the same? Have we learned our lesson?

But the most important economic stories don’t require forecasts; they’ve already happened. And they tend to be the most overlooked, because when everyone’s focused on the future it’s easy to ignore what’s sitting right in front of us.

I want to tell you two of the biggest economic stories that aren’t getting enough attention.

One is that household finances might be in the best shape they’ve ever been in. Ever. That might sound crazy, and it’s easy to overlook because of the second story: Covid has dumped kerosene on wealth inequality in ways we’ve yet to fully grasp.

1. THE NEW BOOM

Near the peak of the Great Depression in 1931, an Ohio lawyer named Benjamin Roth wrote in his diary:

Magazines and newspapers are full of articles telling people to buy stocks, real estate etc. at present bargain prices. They say that times are sure to get better and that many big fortunes have been built this way. The trouble is that nobody has any money.Nobody had any money.

It was an exaggeration, but not much. The economy was broken, and – for years – people were in so much debt and had so little liquid resources that everything just stopped.

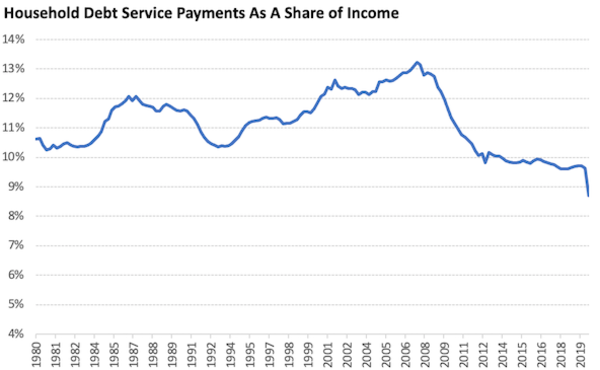

We’re now in our own generation’s Great Depression. But the situation could not be more different from what Roth felt 90 years ago.Take three charts.

Here’s personal income:

Here’s household debt payments:

And personal savings:

Lots going on here. Let’s take it one at a time.

INCOME

Last year was the best year for income in American history. By far. It’s not even close.

A lot of the surge came from stimulus payments and unemployment benefits. But private wages and salaries are back at a new high. So are average hourly earnings. And weekly earnings.

These are not small numbers: Americans made $1 trillion more from March to November of 2020 than they did from March to November of 2019.

The stimulus part of the income equation is the most interesting to me, because it’s so big and has stuck around longer than most imagined.

It’s easy to write off a stimulus payment that boosts income as a one-time lift, not a new level of income that will be sustained or repeated. But that misses how much people love money. And once a new kind of stimulus money is tasted it becomes a permanent feature of how every subsequent downturn is handled.

A lot of the stimulus measures that took place in 2008 and 2020 – from industry bailouts to tax cuts to $1,200 checks – were things most people didn’t think were even possible before they happened. You might give your senator a pass for doing nothing if you think nothing is possible.But now people know these things are possible, so they have a new set of expectations.

No politician can look at unemployed Americans and say, “There’s nothing we can do.” They can only say, “We’re choosing not to do it.” Which few politicians – on either side – want to say when people are losing jobs.

So they stopped saying it.

In 1930, Treasury Secretary Andrew Mellon said, “Liquidate labor, liquidate stocks, liquidate real estate. Purge the rottenness out of the system.”

In 2020, Treasury Secretary Steve Mnuchin said, “We have a lot of money. We need to get that money in Americans’ hands.”

It’s a different world, and you ignore how much has changed at your own expense.

The $1 trillion stimulus package passed last week was a one-day news story, because it’s a fraction of the size of the CARES Act of last spring. A trillion bucks, big deal; that seems like the new view. But $1 trillion is more, even adjusted for inflation, than the 2009 stimulus package that made people’s jaws hit the floor and helped spark the Tea Party movement.

Barack Obama writes in his recent memoir that when he wanted to do a $1 trillion stimulus his own chief of staff responded, “there’s no f**cking way.” It just seemed impossible.

Now we do that and people yawn, and the biggest part of the story is that it’s only $1 trillion when it could have been $3 trillion.

Benjamin Roth noticed the same thing in 1934. He wrote:

People are no longer worried about government spending. An additional billion or two seems to mean nothing. When Coolidge was President in prosperous times he refused to pay the soldiers’ bonus for fear of inflation and the people agreed with him. Today, in the face of unprecedented deficits, the people see Congress approving the bonus and there is hardly a murmur.

Same story, same dynamic, just bigger numbers today.

The outcome in Roth’s day was the birth of Social Security. I wonder if our generation’s response to calamity is an enduring expectation of a thousand-dollar check per household whenever the economy dips.

In any case, the numbers are enormous: Adjusted for inflation, the two stimulus packages passed in the last nine months are roughly equal to what we spent fighting World War II over four years.

It doesn’t matter whether you think stimulus packages and Fed policy are right or wrong or dangerous or immoral – that’s a different topic. What matters is that trillions of dollars have already flowed into households’ bank accounts in ways I don’t think people have come to terms with, because the numbers are so big they’re hard to contextualize.

It helps create a world where tens of millions of jobs are lost, but incomes surge to a new record. It’s a lot of cognitive dissonance to swallow.

DEBT

What do you do when you get a giant stimulus check and you can’t use it to travel because everything’s locked down, or go shopping because the malls are closed, or eat out because the restaurants aren’t open?

Covid has created vastly different points of view, and it’s given people lots of time to sit on the internet.

A hard thing to wrap your head around in economics is the idea that two opposite things can be true at once.

Consumers are in the best shape they’ve been in, ever. A huge portion of consumers think that’s bogus because they’re in the worst shape they’ve been in, ever.

Both are true.

Two different worlds.

*Feature Photo credit: Jp Valery on Unsplash