And for our next trick: Greensill Part 2

So who is holding the bag? Well, genuinely I do not know. It could be Insurance Australia Group or Tokio Marine. It could be German taxpayers (through the subsidiary bank) and Credit Suisse. I figure I know the winners though. Lawyers. Lots and lots of lawyers

Capital Thinking · Issue #800 · View online

There has been much fabulous reporting in the lead-up to the collapse of Greensill, the eponymously named Australian domiciled but London headquartered supply chain financier. But if you want guidance start with anything by Duncan Mavin (from the Wall Street Journal) or Robert Smith sometimes with Olaf Storbeck (at the Financial Times).

The excellent work of these journalists is now on the front page above the fold. It is not everyday a globally significant financial institution fails, and it is rarer still that this collapse happens within a couple of percent of all time highs in markets.

There has been remarkably little coverage of where the losses (which will be enormous) will sit.

Greensill - who is holding the bag?

John Hempton | Bronte Capital:

I do not know either. But I am a short-seller at heart and trying to work this out seems like a core task for me.

I will start my speculations at home in Australia.In late November 2020 I wrote a letter to the Australian Prudential Regulatory Authority (APRA) about the credit risk that Insurance Australia Group was taking on Greensill.

Here is that letter (which given outcomes looks rather on point). This letter is slightly modified, correcting punctuation and having some redactions.

Greensill and Insurance Australia Group

First - you need to know what Greensill and Lex Greensill are.

Lex is a controversial and aggressive factoring/supply chain/trade finance financier. Possibly the most controversial one in the world.

He is an Australian - bought up on a farm near Bundaberg in Queensland - and the parent company is Australian domiciled and still has a Bundaberg address.

The enterprise however is vast - and - by far - the biggest company headquartered in Bundaberg. The official version piles on the humble origins.

https://www.greensill.com/about/meet-lex-greensill/

The unofficial versions focus a little on the indulgences, the family jets etc. Though apparently (and according to one of the articles attached) he is selling the fleet of private jets (four of them) as he takes money from Softbank.

Greensill is controversial. They financed the fraudulent NMC Health.

More publicly they were involved in the collapse of the GAM funds that was widely publicised.In that case the fund manager Tim Hayward overloaded his fund with Greensill paper at valuations some considered questionable.

Since Hayward’s fund collapsed there have needed to be new large-scale sources of finance.

The biggest of these is that Greensill bought control of a tiny (and failing) German bank, recapitalised it, took a huge pile of brokered deposits (by paying about 100-120bps over) and either bought Greensill receivables or pledged bank assets to get letter of credit capacity to support Greensill activities.

The annual report for the bank (alas in German) is attached. The bank assets are largely “insured” but we cannot tell who they are insured by.

What we can see is the Credit Suisse fund that has deep Greensill relations (and is also the subject of this excellent article in the WSJ - https://www.wsj.com/articles/softbank-backed-greensill-looks-to-raise-fresh-capital-11602173906).

I have attached a letter from the Credit Suisse Supply Chain Finance Fund. A good way to start would be to get EVERY letter and prospectus from this fund and any other Credit Suisse fund with a decent Greensill exposure.

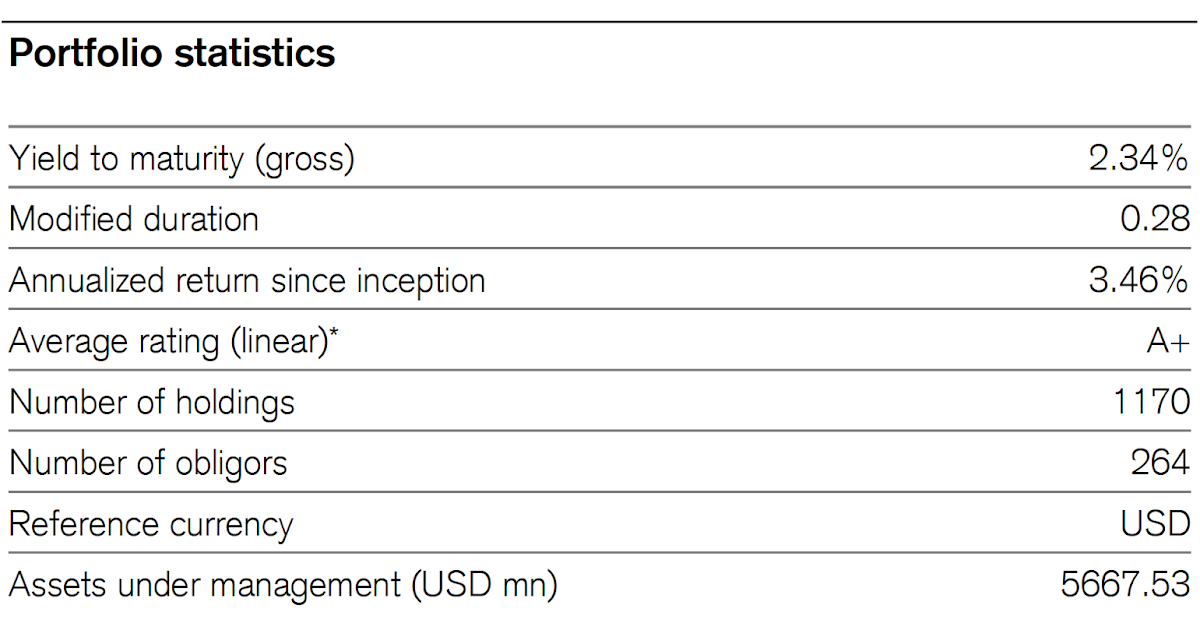

The fund is USD5667 in size - as per this cut-and-paste.

Other than 10 percent US Treasury holding it is diversified as to the countries that the assets are from and the industries that they are in.

But it is not diversified as to the the source of these assets (Greensill, Greensill and Greensill as far as I can tell) or the source of the insurance on these assets.

It is 56.1 percent Insurance Australia Ltd as per the following.

Now that is USD3.18 billion in exposure - just through one fund. That is AUD4.4 billion.

That is just the Insurance Australia exposure I can find.

I am assured the bank assets are also largely insured - but I cannot find who the insurer is.

So you would think that this is a disclosable large exposure to a single controversial financier. But the only statement in the IAG annual report is as follows:

That is it. They say it is in run-off. They feel no need to disclose a multi-billion dollar exposure to a questionable credit/s.

The only problem is that no insurer (other than Tokio Marine) seems to insure for them any more and the amount insured is rising fast.

I think the insurance is written at a broker in Sydney:

https://tbcco.com.au/

This entity used to be owned by IAG and Tokio Marine - but IAG sold their bit to Tokio Marine. However the insured amounts keep going up (at least the bits I can find) even though IAG say the thing is in run-off.

—I have some hypotheses. Either

a) An amount - at least 4.4 billion - but possibly much higher - is insured by IAG. Given the size (say 50 plus billion) and controversy of Greensill this is potentially a solvency risk for IAG.

b). Greensill is faking IAG insurance policies - and the amounts are not insured by IAG but Greensill says they are. In which case the German Bank (taking all those insured bonds) is facing solvency risk - and you should be talking to your German counterpart.

c). The Credit Suisse documents are fake. I think this unlikely but cannot dismiss it.

Either way it is one of the uglier situations I have seen lately.

John

APRA (and to the extent I talked to them the Australian Securities Commission) dealt with me professionally. I was originally not short any company mentioned, but I did not want to restrict my ability to trade.

They asked me a few precise questions but gave me no indication as to whether they took these issues seriously or what they were thinking. I wanted no insight to their thoughts and they gave me none.

But Sarah Danckert in the Age has reported (quoting multiple sources) that APRA has been interested in the situation since November. So I guess my letter had the desired effect although for all I know APRA may have already had the situation in-hand.

Anyway it is clear that IAG had a large and thinly disclosed Greensill risk.

The collapse of Greensill and the role of the insurers

Tom Braithwaite in the Financial Times (and others) have reported that the proximate cause of the collapse of Greensill was that these insurance policies were not renewed.

This led to a chain of events whereby Credit Suisse funds stopped accepting Greensill assurances and BaFin (the German regulator) took over Greensill Bank.

The best bits of information however come from an Australian court case.

Late at night and in emergency sitting the Supreme Court of NSW (a first-instance court despite its title) heard an urgent after-hours application for an interlocutory mandatory injunction compelling insurer to issue a trade credit insurance policy.

This was always a long shot.

The policy terms require 180 days notice to terminate or the insurer might be forced to renew. The argument Greensill made to the court was that maybe 179 or 178 days of notice was given, not 180 days and that Insurance Australia Group should be forced to renew USD4.6 billion in credit insurance for which it had no reinsurance coverage.

Understandably at a last-ditch 7PM hearing a single judge wasn’t prepared to bankrupt a major Australian insurer by forcing renewal.

You can find the judgement here.

Greensill duly collapsed as they told the Judge that it would.That said, the question of whether Greensill can force renewal of those policies is still open and is still going to court.

All the judge decided was that at short notice and on only an “arguable” case he wasn’t going to issue a mandatory injunction. So there will be a court case to come. And the court case will reveal new details and make important decisions.

The alleged rogue underwriter and what is at stake?

John Hempton

John Hempton

Photo credit: William Daigneault on Unsplash