Like John Malone on steroids

“I’m spoiled – it’s terrible, I’m used to living a good lifestyle, and I’m a very big spender.” -Bill Foley

Capital Thinking • Issue #1098 • View online

Bill Foley is one of the most interesting billionaires you’ve probably never heard of. Despite his massive success and extraordinary business acumen, there’s relatively little written about him.

We first got interested in Foley because we were taking a look at the title insurer Fidelity National Financial (FNF for short). FNF is Foley’s baby, which he built from the ground up to be the dominant title insurer in the US.

Bill Foley

It turns out that Foley is John Malone on steroids, which is to say he is one of the most active deal junkies you’ll ever come across (like Malone, he’s also a pirate 😉), so this is far from an exhaustive profile.

We’re just selectively sharing what we found interesting.

How Foley got started

Fast forward to when Foley was ~30 years old. He had just finished law school and joined a law firm in Arizona.

Foley is one of those people who cannot work for somebody else, so after only two short years in the industry he started his own law firm, Foley, Clark & Nye, in 1976.

During this time, he was handling the legal work for a local savings and loan company, SS&L. He became a major investor in SS&L and joined it full-time in 1981.

While working for SS&L, he helped them acquire a small title agency as well as a small title insurer, FNF. The strategy was to cross-sell SS&L’s banking services to title insurance customers.

Foley and Frank Willey (who worked at Foley’s law firm) began rolling up small title companies across California on SS&L’s behalf. FNF’s revenue grew quickly over the next three years, from $6M to $40M.

Foley had some gripes with SS&L (including with their lax underwriting, which eventually resulted in their bankruptcy during the savings and loan crisis) and thought that FNF had huge potential that was not being exploited properly. He formed an investor group to purchase FNF from SS&L in 1984 in a $21M LBO.

Foley’s equity check must’ve been quite small as most of the purchase price was vendor financing by SS&L. An old newspaper article seems to suggest that he bought FNF for just ~0.5x P/S and less than book value. Foley left his law practice that same year to become Chairman and CEO of FNF.

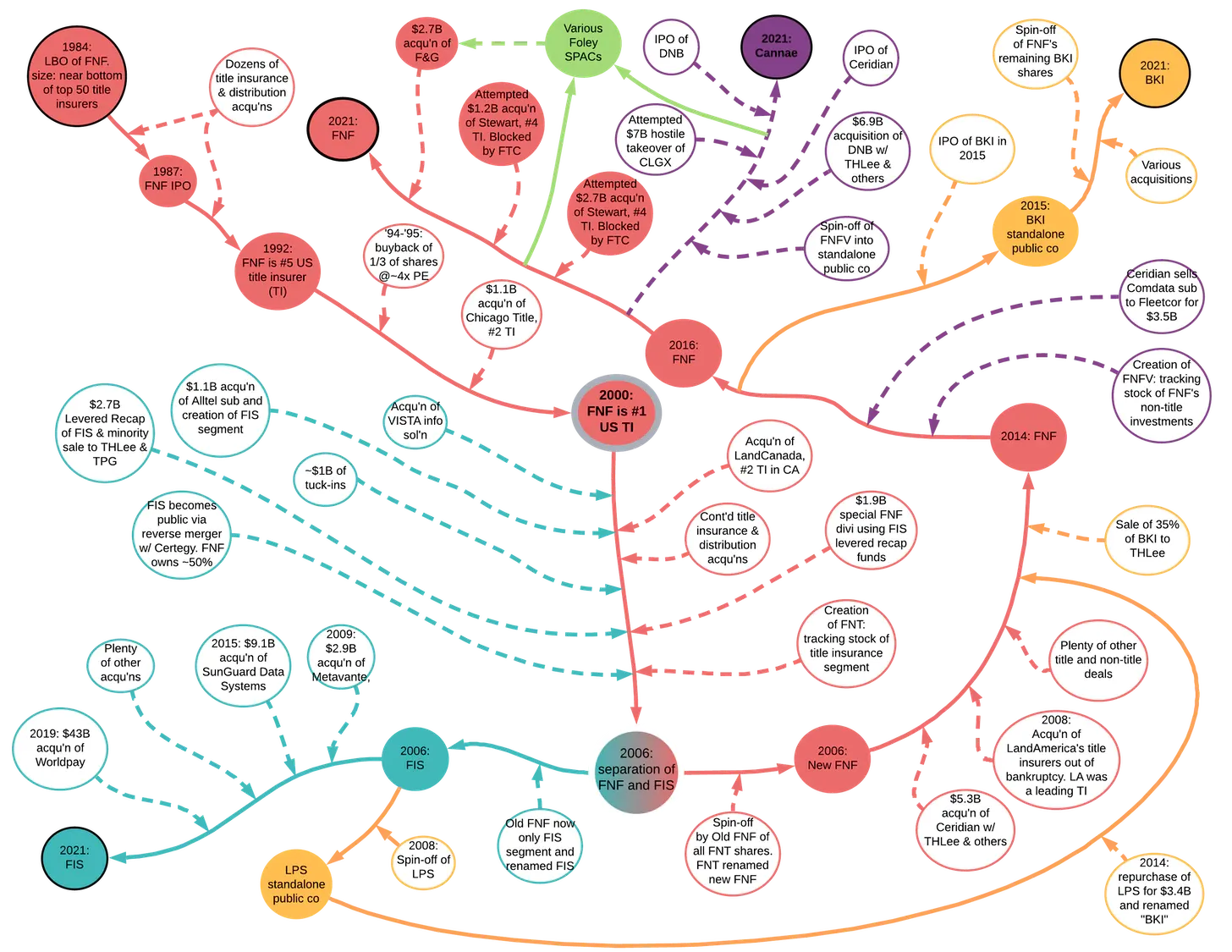

A Deal Junkie

Believe it or not, the chart above is a highly abbreviated version of Bill Foley’s deal making history. It excludes dozens if not hundreds of deals.

The “Recent Developments” section of the old FNF annual reports was usually a multi-page affair, before FNF got so big that the materiality threshold began to cloak the ferocious deal making.

Every year of FNF history is a real trip… just when you think you know what’s going on, he starts issuing LYONs (we had never heard of them either: Investopedia) and buying them back again at a gain, buying the high yield bonds and wiping out Buffett’s equity at auto parts maker Remy International1, or investing in timberland assets.

Beyond the insatiable deal-making at his public companies, he’s made many private investments across wineries, golf courses, hotels, ski resorts and restaurants, among others.

Back in the ‘90s and early 2000s, his “side hustle” aside from running FNF was to roll up struggling QSR chains at CKE Restaurants, a public company at the time.

He’s also built an NHL expansion team from scratch over the last several years (Vegas Golden Knights), taking it to the Stanley Cup finals in its first year.

That’s why we said John Malone on steroids…

Track Record

How well would you have done had you hitched your wagon to Foley by investing in the 1987 IPO of FNF, held onto all the spin shares you received along the way and reinvested all the dividends?

You would have compounded at around 19% per year over the last 34 years.

A 350 bagger.

Barry Diller’s IAC has compounded at 15% from 1995 to today, over which time period Foley has also done ~19% a year. The S&P 500 compounded at ~10% per year over that time period.

Needless to say, it’s a spectacular track record that makes Foley one of the best investors of the last 3-4 decades.

Foley has become a billionaire despite his humble beginnings of being born into a middle-class family. His stakes in public companies are worth ~$1.7B (FNF, FIS, Cannae, BKI, DNB, and various SPACs).

Beyond that he owns many other assets including a majority stake in the Golden Knights (the franchise cost ~$500M and is valued around $750M-$1B).

Title Insurance as a Platform

The four large title insurers in the U.S. are cash cows today. It’s an oligopoly with significant barriers to entry and scale as well as high returns on tangible equity.

We may write up FNF in the future, but for now you can check out these VIC write-ups if you’re interested in the basics:

https://www.valueinvestorsclub.com/idea/FIDELITY_NATIONAL_FINANCIAL/4885281745

https://www.valueinvestorsclub.com/idea/FIDELITY_NATIONAL_FINANCIAL/1790653413

The industry didn’t look anything like this when Foley bought FNF. The industry was quite fragmented with slim margins.

Of course, that was part of the allure for Foley. Foley recognized that title insurers could be bought on the cheap yet had some very attractive attributes:

- Non-discretionary: mortgage lenders require end customers to get title insurance. Virtually every real estate transaction in the U.S. involves the issuance of title insurance.

- Purchased by agents: real estate agents and loan officers are the primary gatekeepers in the real estate purchase/refinance process. They steer end customers towards a title insurer. However, they’re not the ones paying for the policy. For example, one of us bought a condo recently and the lawyer involved in the closing process simply chose the title policy (confession by the buyer: I didn't even remember the name of the title company until looking into my files for this project). It is illegal for title companies to pay realtors commissions to steer clients to them. This entrenches FNF, the scaled player, as they can maintain relationships through indirect means, such as cross-selling software to realtors, having by far the largest national sales team that does nothing but call on realtors, and aggressively hiring away rainmakers from smaller firms.

- Low cost-to-value: title insurance premiums are tiny relative to the value of real estate transactions. We’re talking about basis points. This is a positive, both for pricing power and a lack of price shopping by customers.

- A royalty on US real-estate: Title insurance is generally priced as a base fee plus a % of the value of the property. Real estate is an asset class that appreciates over time which provides automatic price increases for title insurers.

- Insurance of past rather than future events: title insurance protects against events in the past that are often knowable (undisclosed deed against the property, unpaid property taxes, undisclosed co-owner etc.) rather than unknowable future events such as inclement weather. Thorough underwriting due diligence leads to very low loss ratios (~4%-5% loss rates) which makes title insurance unlike other types of insurance. Title companies are not really insurers as much as they are real estate transaction processors.

These industry attributes helped FNF become a great business over time as the industry further consolidated. Foley was also keenly aware that most title insurers were sleepy companies run by unimaginative management teams.

By running the business much more cost efficiently than competitors and changing up a few industry conventions, especially around distribution, he vastly improved the economics.

While FNF’s economics back then looked far different from today, it was already a 20%+ ROE business, so Foley had plenty of cash flow coming in to plow back into the roll-up.

While cyclical, the business could still carry some leverage, giving Foley yet more fuel for acquisitions. The third leg of the stool were the public markets.

Foley took FNF public after just three years of ownership, in 1987, and was a big issuer of stock for acquisitions (by our math, FNF’s shares outstanding went up about 7x between 1993 and 2013, adjusted for stock splits and stock dividends).

Owning the Distribution

Arguably the most important change Foley and Frank Willey made at FNF was to pivot the business towards direct distribution.

Historically (and to this day), title insurers relied on independent agents, not unlike many other types of insurers.

Title insurance on its own can be a relatively commoditized product. The excess returns in title insurance, in part, come from controlling the local relationships with hundreds of thousands of brokers, lawyers and loan officers across the country.

This is why to this day, despite a much more consolidated title industry, local independent title agents retain 70%-90% of the premiums they originate, passing on only a small fraction to the title insurer.

Foley recognized this and aggressively rolled up independent agent firms.