Death of a Business Model

It took thirty years for the volume of telegram transactions to halve, and the same amount of time for the number of horses to halve. It’s a long, slow process.

By Capital Thinking • Issue #887 • View online

It normally takes a lot less time to destroy a thing than to create it.

That’s true on building sites, in careers and of reputations. “It takes 20 years to build a reputation and five minutes to ruin it,” said Warren Buffett.

Such is the nature of entropy.

The Long Slow Short

Marc Rubenstein | Net Interest:

Yet in business, the reverse can often seem the case.

It’s never been easier to start up a new company. In the US, business formation is running at the highest level on record.

Companies can be spun up from idea to $2 billion valuation in the space of fifteen months. And, at the larger end of the scale, Facebook is a reminder of how quickly value can be created – this week, it became a $1 trillion company after being around for just seventeen years (I have cardigans older than that!)

These companies open new markets and/or promise to disrupt existing ways of doing things.

On the other side though, the incumbents they disrupt can often hold on for a lot longer than anyone thinks possible. Kodak, Blockbuster, Sears – they all took years to be put out of their misery.

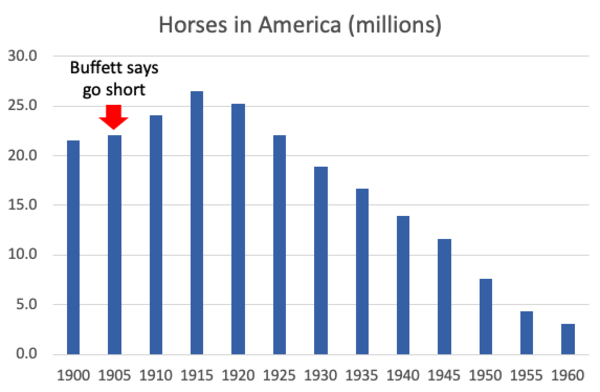

Warren Buffett makes the observation about autos that,

“what you really should have done in 1905 or so, when you saw what was going to happen with the auto is you should have gone short horses. There were 20 million horses in 1900 and there’s about 4 million horses now. So it’s easy to figure out the losers, you know the loser is the horse.”

But you would have needed a lot of staying power to have been short horses.

Historic horse prices are hard to come by but, using Buffett’s proxy, the number of horses stayed above 20 million for a further 25 years after he says you should have gone short.

One of the reasons there’s a lot more money in venture than in short-selling is precisely because it can take so long for a business to destruct.1

A good example of this on the periphery of financial services is Western Union.

I was short the stock once on the Buffett principle that it is easier to identify the loser than pick the winners – in this case in digital payments. I underestimated two things – one, how long the market shift would take to occur; and two, how much free cash flow Western Union would generate along the way.

Actually, there was a third factor that I’ve only recently understood: this is a company that peaked in 1878. My short wasn’t exactly a novel idea!

Faced with disruption from the telephone, the fax, the personal computer, the internet, and now digital payments, Western Union has been on a steady decline for over 140 years.

When it comes to operating in markets that are collapsing around it, Western Union has form. And yet it’s still going.

This is the cautionary tale of Western Union.

Photo credit: Sandra Tan on Unsplash